Analyst Highlights

- Equities: US stocks were mixed as S&P 500 dipped 0.5% and Nasdaq fell 0.9%, while Russell 2000 rose 1.6%, signaling rotation toward small-cap value.

- Rates: Treasuries sold off as Trump’s Fed-chair signals lifted Warsh odds, trimming 2026 cut bets and pushing the 10-year yield up to 4.22%.

- Crypto: Risk appetite improved as Bitcoin gained 4.5% and Ether jumped 8.0%, supported by the biggest Bitcoin ETF inflow since October (~$760M).

- Commodities: Metals outperformed with silver up 4.6% while gold slipped 0.2%; oil was steady-to-mixed as Brent edged higher and WTI eased.

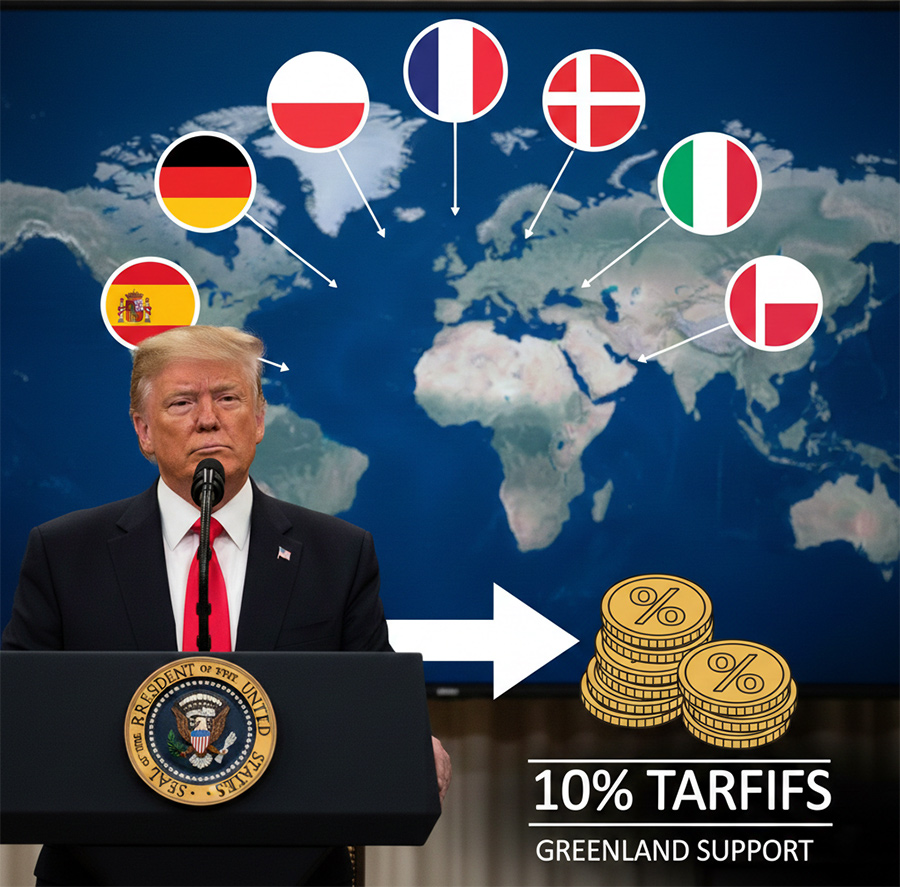

- Geopolitics/Trade: Trump’s Greenland-linked tariffs on eight NATO allies raised EU retaliation risks and weighed on Europe’s risk sentiment into the open.

- Tech/AI: Capital formation stayed aggressive with Anthropic’s reported $25B raise push, Skild AI’s $1.4B round, Meta smart-glasses scaling, and Micron’s $1.8B Taiwan fab deal.

IPO’s in the week

- Green Circle Decarbonize Technology Ltd (GCDT, NYSE American) — A Hong Kong–based decarbonization and energy-efficiency technology company providing phase-change thermal energy storage (PCM-TES) solutions for HVAC and cooling systems, priced its IPO at $4.00 per share on January 13, 2026, offering 5 million shares to raise $10.0M to support commercialization and expansion of its energy-saving technologies across Asia and the Middle East.

- OneIM Acquisition Corp. (OIMAU, Nasdaq Global) — A Cayman Islands–incorporated blank-check company (SPAC) sponsored by an affiliate of OneIM, a global alternative investment manager, priced its IPO at $10.00 per share on January 14, 2026, offering 25,000,000 shares to raise $250.0M to pursue a merger or business combination across industries.

- FG Imperii Acquisition Corp. (FGIIU, Nasdaq Global) — A Cayman Islands–incorporated blank-check company (SPAC) targeting an initial business combination, with a primary focus on North American financial services, filed to price at $10.00 per share, offering 20,000,000 shares to raise $200.0M for a future merger or acquisition.

- Infinite Eagle Acquisition Corp. (IEAGU, Nasdaq Global) — A Cayman Islands–incorporated blank-check company (SPAC) seeking a merger or business combination, with no stated industry or geographic focus, filed at $10.00 per share with 30,000,000 shares to raise $300.0M, aiming to leverage the team’s global relationships and operating experience.

Markets Weekly

- S&P 500 closed at 6,940.01, down 26 points (-0.53%) for the week.

- Russell 1000 (IWB) closed at 44, down 1.76 points (-0.46%) for the week.

- Russell 2000 closed at 2,677.74, up 05 points (+1.59%) for the week.

- Russell 3000 closed at 3,954.54, down 81 points (-0.37%) for the week.

- CBOE VIX closed at 86, up 0.74 points (+4.9%) for the week.

- Dow Jones closed at 49,359.33, down 87 points (-0.47%) for the week.

- Nasdaq Composite closed at 23,515.39, down 51 points (-0.92%) for the week.

- Bitcoin closed at $95,270.98, up $4,077.99 (+4.47%) for the week.

- Ethereum closed at $3,338.31, up $245.98 (+8.0%) for the week.

- Solana closed at $142.38, up $3.24 (+2.3%) for the week.

- XRP closed at $2.0565, up $0.0040 (+0.19%) for the week.

- Gold closed at $4,595.40, down $8.90 (-0.19%) for the week.

- Silver closed at $88.54, up $3.93 (+4.6%) for the week.

- WTI crude closed at $59.34, down $0.16 (-0.3%) for the week.

- Brent crude closed at $64.13, up $0.26 (+0.4%) for the week.

- Treasuries fell as Trump Fed-chair remarks boosted Warsh odds, trimming rate-cut bets; 10-year yield rose to 22%.

- China rare-earth exports fell in December as tensions with Japan raised scrutiny on potential shipment controls, highlighting Beijing’s leverage in strategic materials.

- European stocks face pressure as Trump’s Greenland-related tariff threats weigh on risk sentiment, with EU retaliation risks rising.

- Bitcoin ETFs saw their biggest inflow since October’s crypto crash, pulling in about $760M as Bitcoin rose ~10% YTD and Ether also rallied.

- Bank of Japan will begin selling its ETF and REIT holdings next week, starting at about ¥330B per year.

Politics Weekly

- Trump administration moves to reshape the Fed as Powell faces a DOJ probe over HQ renovations; Trump expected to name a successor soon.

- Trump imposed 10% tariffs on eight NATO allies over Greenland support, threatening a hike to 25% in June unless a purchase deal is reached.

- Carney said Canada is concerned by Trump’s Greenland escalation, backing Denmark and Greenland’s sovereignty and framing Arctic security as a NATO responsibility.

- Carney called China a more predictable trade partner than the US, widening the policy gap as Canada opens EV quotas and Chinese auto investment.

- Canada allows limited Chinese EV imports, diverging from US policy; auto executives warn of supply-chain erosion and job losses.

- EU Parliament weighs delaying/conditioning approval of a US trade deal unless Trump drops Greenland takeover threats; lawmakers split, raising fresh uncertainty.

- EU and Mercosur signed a landmark free-trade deal after 25 years, creating a 700M+ consumer market; ratification still pending.

- Iran’s Khamenei acknowledged “thousands” killed in protests, blaming the US; Trump called for new leadership as unrest and crackdown intensify.

- Brazil’s Lula condemned Trump’s Venezuela operation as undermining sovereignty and international law, warning it could destabilize trade and trigger refugee flows

Technology Advancements in the week

- Sequoia plans major Anthropic investment as startup seeks $25B raise at $350B valuation; GIC and Coatue reportedly add $1.5B each.

- Skild AI raised about $1.4B, valuing the robotics startup above $14B, to scale its “Skild Brain” robot software and deployments across environments.

- Meta and EssilorLuxottica are discussing doubling Ray-Ban AI-glasses output, targeting 20M+ annual capacity by end-2026 as demand surges.

- ServiceNow agreed to buy cybersecurity startup Armis for $7.75B, its largest deal, to expand cyber capabilities by integrating Armis threat data.

- Micron signed an LOI to buy Powerchip’s P5 fab site in Taiwan for $1.8B, expanding DRAM capacity with phased ramp from 2Q close.

👉 Keep the conversation going! Subscribe to our weekly newsletter for more insights, delivered straight to your inbox.